Does Cravath Have A Drafting Accent?

Using the Oxford Comma as a Drafting Fingerprint

It’s worth knowing before we get into this week’s substack that I was motivated to write it after I told someone that “I’m done dinner.” I then got made fun of because this is a stigmatic phrase of the Philadelphia accent. And, it’s true, I’m from Broomall, PA, right next to murdur-durduring Mare of Easttown. I can’t tell you how many students have laughed at my pronunciation of gazz.1 What can I say, I represent my heom.

In all events, the incident got me thinking about legal accents. And I wondered if law firms have their own syntactic fingerprints, like justices. Or law professors, I guess.2

The obvious place to look is the Oxford Comma debate, since lawyers love arguing about it. Plus, in 2017, in O’Connor v. Oakhurst Dairy, a Maine dairy lost a class action over overtime pay because the Maine legislature was no Oxford comma celebrant. A state law had exempted workers involved in “the canning, processing, preserving, freezing, drying, marketing, storing, packing for shipment or distribution of” perishable foods. Without a comma before “or distribution,” it was (allegedly) unclear whether “packing for shipment or distribution” was one activity or two. The ambiguity ultimately cost Oakhurst Dairy about $5 million.

Lawyers—like M&A savant Glen West—pounced, noting that the absence of commas can cause oversized troubles. And yet others, like noted drafter Ken Adams, disagreed.

This suggested to me a fun project. Like preferences for Equity, or Garamond Premiere Pro,3 I see the serial (Oxford) comma as a style choice — “A, B, and C” versus “A, B and C.” It carries no intrinsic legal meaning of its own. So, if a drafter consistently picks one over the other, that’s a fingerprint of how they write, not what they mean. Which produced a testable question:

Can you tell which law firm drafted a merger agreement just from its commas?

Let’s give it a shot.

The Corpus

The dataset is the same as last week’s. I pulled 13,957 merger agreements filed on SEC EDGAR between 2000 and 2026, for both public- and private-targets. And then I used Claude Code to identify what I’ll call serial comma opportunities within the body text of each agreement: a list of three or more items joined by a final and/or/nor, where the slot right before that last conjunction either has a delimiter (serial) or doesn’t (non-serial).

I detected these opportunities three ways, from most to least reliable:

Enumerated lists —

(i) … (ii) … and (iii) …Semicolon series —

A; B; and C.Prose lists —

A, B, and C.

This yielded 11.8 million comma decisions. From these (after lots of false starts and auditing) I got to something like 93% precision identifying what I believe to be Oxford Comma possibilities.4 With that denominator in hand, it’s simple enough to ask: are our M&A lawyers Oxford partisans?

They are not.

M&A lawyers overwhelmingly skip the Oxford comma. Consider the common phrase “representations, warranties[,] and covenants”. It shows up nearly 8,000 times across the corpus — in about 4,300 of the 13,957 agreements — and 93% of those times there's no comma before ‘and.’” Some firms use it zero percent of the time.

On first glance, this might sound like the end of the project: if essentially the whole M&A bar defaults to no-comma, what’s left to fingerprint? But the dialect was never going to be the level of use of this syntax, it’s rather firms’ unique lean against the mean. So I asked if the lean consistently differentiated the firm.

Whose Pen?

Before I can pin an accent on a firm, I have to know whose hand actually held the pen. By convention, the buyer’s counsel drafts the merger agreement. I identified each deal’s acquirer-side firm — from the “copy to” line of the notices clause, normalized against a dictionary of M&A shops — and assigned it as the drafting_firm.

But a merger agreement is typically negotiated; the other side marks it up. So is the comma style really the drafter’s?

I tested this by decomposing the variance of each document’s comma rate between the buyer’s counsel and the target’s counsel:

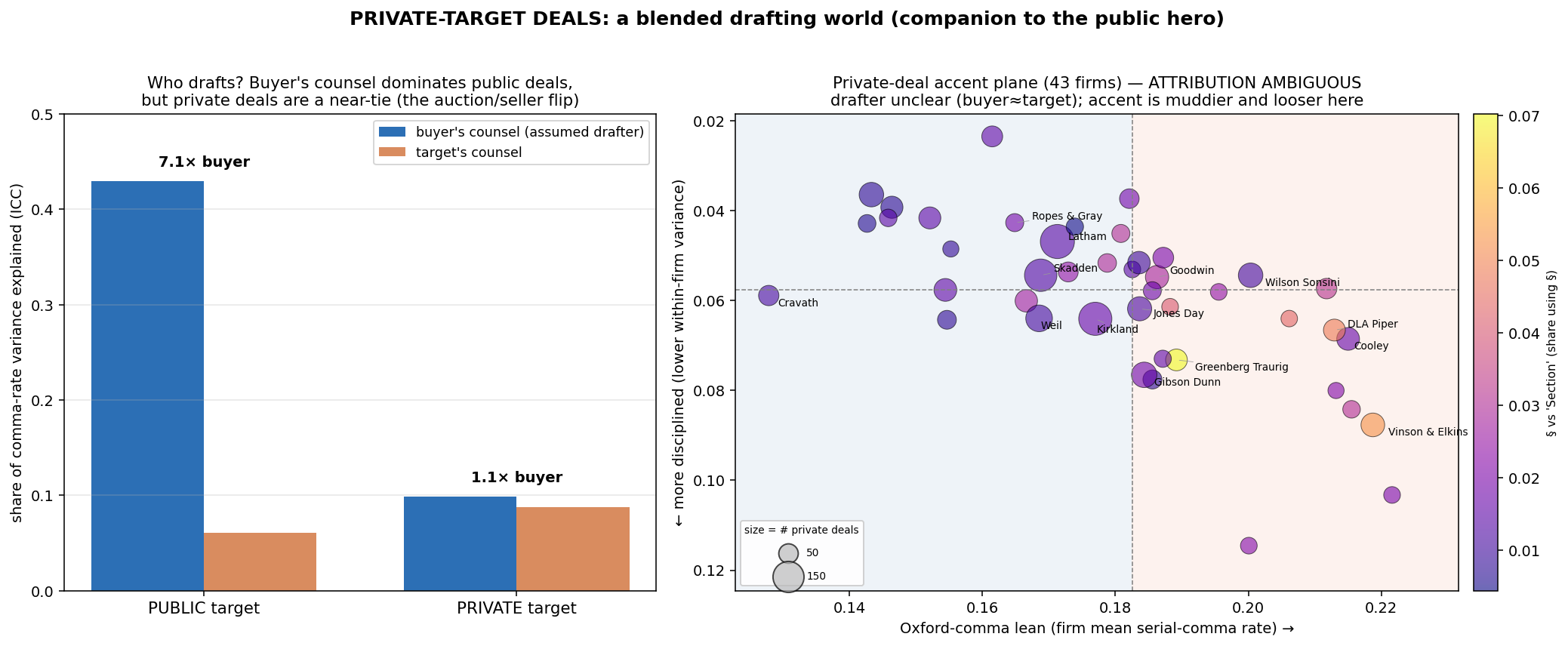

Public-target deals: the buyer’s counsel dominates ~7-to-1. The document carries the drafter’s accent, and attribution is clean.

Private-target deals: it’s a near tie (~1.1-to-1). Here the convention breaks — in private and auction sales the seller’s counsel often drafts to control the process, so “who drafted” is genuinely ambiguous.

What this told me was that the private deals were the more complicated half of the dataset, and the signal there is too tangled to attribute. So for the rest of this post I’m looking only at public-target deals, where the comma we see really does belong to the firm we think wrote it. I lop off about half the data and focus on ~6000 deals that are public.

Attributing the Drafter

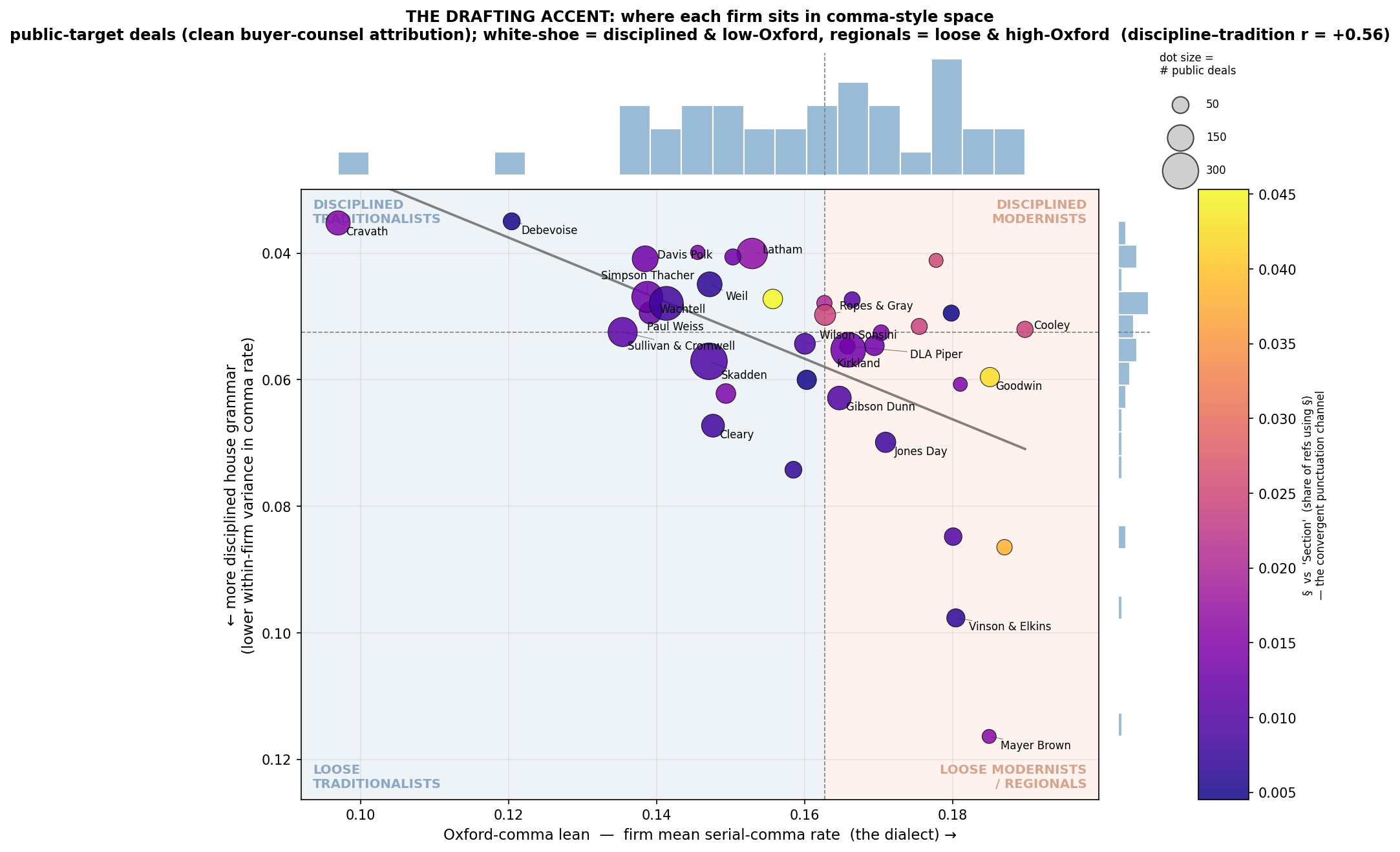

Looking just at the public-target deals,5 the drafting firm explains about 12× more of a contract’s serial-comma rate than the filing year does (firm ICC ≈ 0.55 vs. year ≈ 0.045). Style clusters by who, not when.

Here is the key finding in visual form— each firm placed by its Oxford-comma lean compared to the mean firm (the dialect) and its internal discipline (how consistent it is across deals, not within any one of them). I also use color to show whether these firms as buyers’ counsel tend to spell out “Section” (darker) or use “§”. My theory was that this, too, was stigmatic. And it mostly was.

Cravath sits at the extreme: the lowest Oxford-comma rate and the tightest discipline. The white-shoe bar (Davis Polk, Sullivan & Cromwell, Wachtell, Simpson Thacher, Paul Weiss, Debevoise) clusters as both internally disciplined and low-Oxford, and tends to spell out “Section”; regional and tech-era firms (Cooley, Vinson & Elkins, Mayer Brown) run looser, higher-Oxford, and use “§”. The volume giants (Skadden, Kirkland, Latham) sit in the undistinctive middle. And Mayer Brown is both generally pro-Oxford and very permissive of differences within the firm.

The accent maps onto firm lineage: the traditional Wall Street firms barely use the Oxford comma and apply that style with remarkable consistency, while newer and regional firms use it more, and more variably.

Very sadly for my dream of winning the Nobel Prize in applied linguistics, none of this lets you pull a fingerprint from a single contract. Using comma usage in one agreement to guess at a firm turns out to be close to a coin flip of a problem. The firm’s syntax is a faint, stable impression that you can pull only if you average hundreds of decisions across its whole body of work.6

Does the Accent Reflect Grammar, or Merely Boilerplate?

Thinking about this a bit more, a firm could look consistent for two very different reasons. It could be a house grammar — presumably built on a style guide that its lawyers execute on. Or it could be a house form — a template, copied deal to deal.

Now, I worked at Cravath a long time ago, even before the firm earned its LLP. It then had and enforced a style guide. (I still indent my addresses the way I did in 2002.) But the problem is that grammar and form could both produce what we just saw.

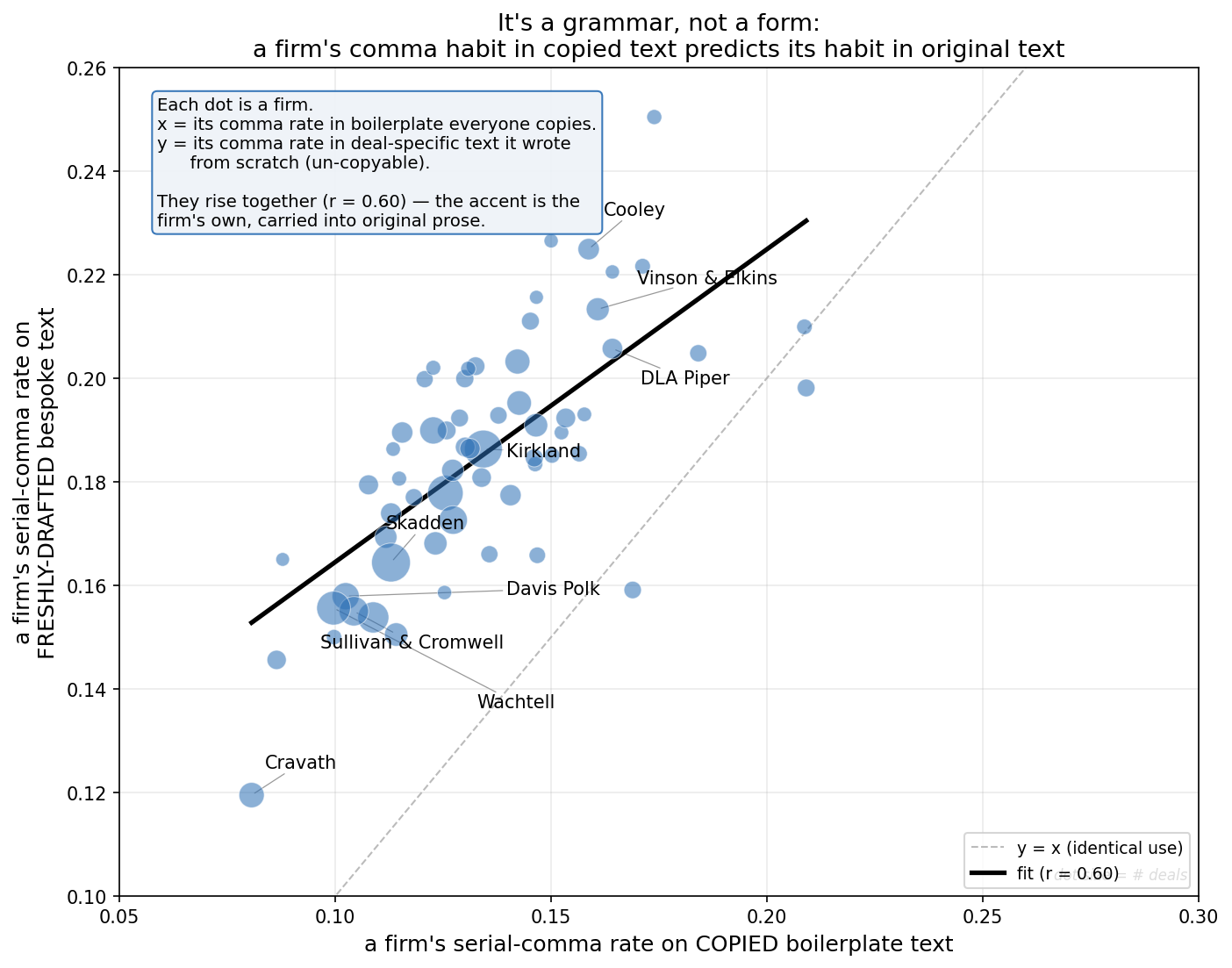

I tried to separate the possibilities by asking Claude to distinguish text that is unique to the deal from text that is the same deal to deal. I normalized each list down to its bare words — lowercased, numbers and punctuation stripped, so near-identical phrasings collapse to one key. Then, for each phrase, I coded how many different merger agreements in the whole corpus contain it.

Thus, “representations, warranties[,] and covenants” turns up in thousands of documents: that’s boilerplate, lifted from shared precedent.

A list of one target’s actual product lines, or its specifically named subsidiaries, appears in exactly one document — the merger before us: that’s bespoke, written for that deal and that deal only.

I labeled phrases found in 25 or more documents as boilerplate, phrases unique to a single document as bespoke, and then measured each firm’s Oxford-comma rate separately on the two piles. The logic is simple: a firm can inherit a comma from a copied form, but a comma in a sentence that exists in only one contract in the country had to come from whoever was dictating that day.

A firm’s comma rate in boilerplate predicts its rate in bespoke text (r = 0.60) — the accent shows up when the firm is writing from scratch, where no template could have put it. I’d identify it therefore as grammar.

There’s a second, independent reason the template story doesn’t hold, which I’ve put in the notes: when you measure how much more a firm’s own documents resemble each other than they resemble everyone else’s from the same era and deal type, the answer is basically zero. But I confess that this result makes me a bit uneasy so I don’t want to press on it hard.7

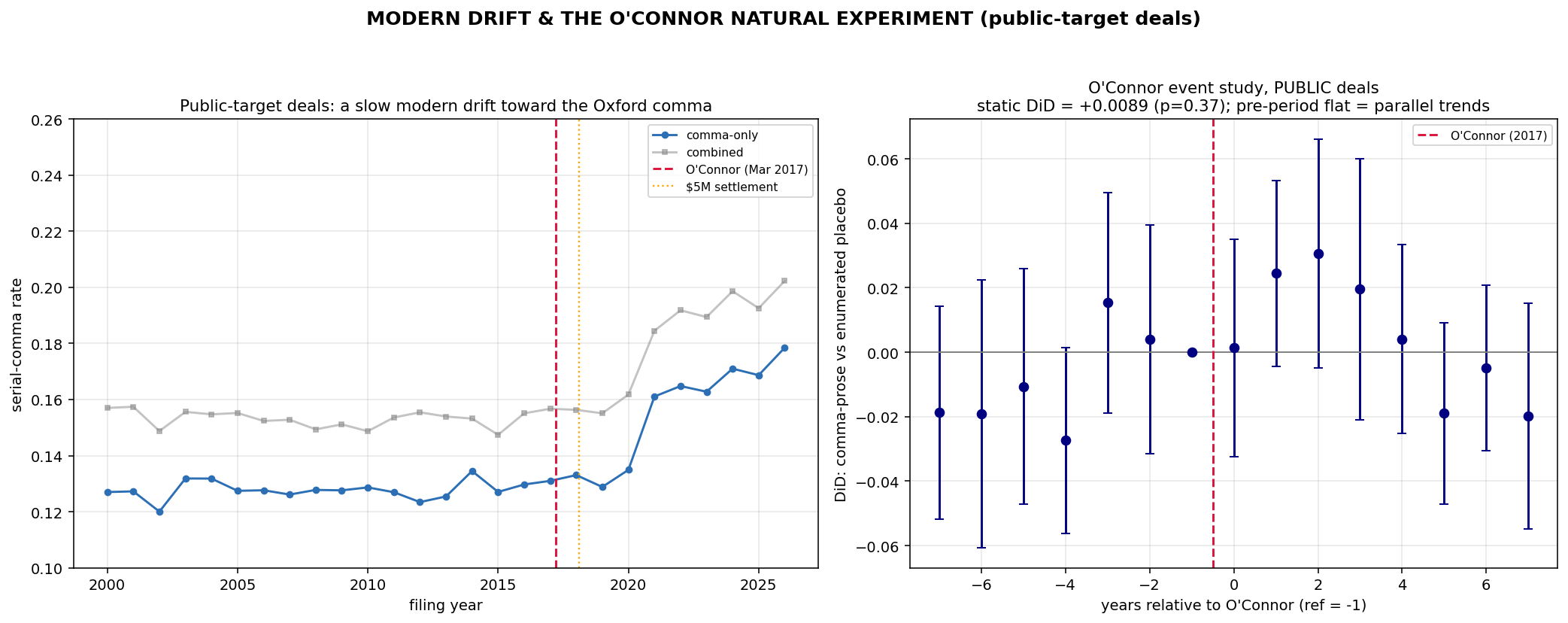

The Oxford Comma Over Time

Even if you think they are annoying and have confused an aesthetic preference for a linguistic rule, the Oxford comma people are winning.

Two things here. First, post-2020, lawyers use the Oxford comma a lot more. I have no idea why. Maybe remote work pushed people to be more online, where they got infected by the serial-comma influencers. But it’s definitely not because of the O’Connor case I started with — though you can bet I tried to make that fetch happen.8

Some Concerns, Musings[,] and Extensions

I did all this in a few hours with Claude Code, coming up with ideas to test and having it execute with lots of supervision. That’s dangerous, because I don’t know what Claude doesn’t know and vice versa.9 And some of these analyses are complicated! If this was a real piece of scholarhip, I’d be co-authoring with someone who knows what they are doing. The goal today was to simply generate some ideas and play with them, not to produce the last word.

Directionally, though, it should be right: the Oxford comma can be a small window onto a big fact about elite legal drafting. There’s plenty of evidence that drafting is both a production process and a craft tradition, particularly in elite NY firms. That tradition has a grammar, transmitted person to person, recognizable in the aggregate, applied with discipline presumably through in-house guardians of the style guide. In other firms, that firm-wide craft tradition has less purchase, and at the same time everyone slowly drifting toward the Oxford-comma monoculture. This probably results from lateral partner movement, just as geographic movement and social media is killing our regional dialects. (You, though, can pry my wooder from my cold, dead hands.)

And, finally, there’s Cravath, which is actually pretty distinctive even among white-shoe firms. There are obviously lots of reasons for its strong internal drafting culture — the firm’s long-held, but now fading, resistance to outside talent, its relatively small size, its partner-team-structure, and the font. So maybe Cravath’s syntactic style is just an anachronism. Another telex fossil, ready to be smoothed away by AI drafters.

But, at least by hypothesis, we should probably guess that the firm’s internal controls are serving clients as well as building firm culture. Which got me wondering whether a firm’s syntactic accent could be driving value in deals — since quite possibly firms that are focused on style are also careful about avoiding drafting errors that matter.

I’ll leave that question—which will challenging to make progress on—to a different post. Or maybe even a real paper.

Gasoline, employed in economic duress arguments to show the hopelessness of solutions internal to contract law.

My style is footnote forward. My comma practices are inconsistent as a warranty of human-centered drafting. And I spell judgement with the e it was born with.

Equity is amazing. Garamond Premiere Pro has gained fame in recent years because it is the preferred font of a few law professors who are extremely smart and productive, and as a consequence of those attributes place in top journals. Faculty believe that the font is causing the placements. It is probably not. Equity Font, however, causes people to believe you are more thoughtful than you are. It is the way.

This is deceptively hard: two-item lists (no opportunity), appositives (“owned, directly or indirectly, by”), date commas (”December 31, 2022, and”), and the big one — commas that join clauses rather than list items (”…incurred in this transaction, and neither party shall…”). Each of those, left unhandled, fakes an Oxford comma.

Using a crossed random-effects model. A crossed random-effects model treats firm and year as two overlapping groupings — every contract belongs to one firm and one year, and firms span many years while years span many firms — and estimates how much of the variation in comma rate each grouping explains. I use random effects (not fixed) because the question is about variance shares, not any one firm’s coefficient, and because it sensibly shrinks the estimates of firms seen only a handful of times.

I tried to decompose the variance of an individual comma decision and 97% of it is within documents — every contract is internally a near-coin-flip, mixing serial and non-serial lists constantly. Only ~0.8% is between firms. The firm signal is a faint, stable bias on top of an enormously noisy process. Average hundreds of decisions over a whole contract and that bias surfaces (hence the firm clustering). But look at any single contract and it’s drowned out.

And the rival explanation — recycled forms — doesn’t hold. A firm could look consistent simply because it rinses and repeats one house template. This churn idea would be consistent with the important finding from Rob Anderson and Jeff Manns paper on poison pills. But I parsed each agreement into a fingerprint of overlapping character sequences and measured how similar a firm’s documents are to each other, then subtracted how similar they are to other firms’ documents from the same era and deal type. If a firm leaned on a proprietary form, its own documents would be far more alike than that baseline — a large positive “excess similarity.” A histogram of that number across firms would have piled up well to the right of zero. It didn’t: it sat squarely on zero (mean −0.02; no firm above +0.09; several slightly negative). At least on this measure, merger agreements are near-duplicates of one another across the entire profession — the templates belong to the bar, not to any one firm. “Form,” then, cannot be what separates Cravath from Cooley.

I tried using a within-data placebo: enumerated `(i)/(ii)/(iii)` lists, which are unambiguous regardless of the Oxford comma. If the case mattered, prose lists should rise relative to that placebo.

And…there’s a transient bump in 2017–2019— suggestive — but it fades, and the controlled effect is not statistically significant (+0.009, p = 0.37). Meanwhile the real shift is a broad jump around 2020, three years after O’Connor and visible across all list types, including the placebo.

I did some independent coding and found that precision of the serial comma was a little bit above 90%: the detector is real bad with prose serial calls (clause-joining “and”s that mimic a list comma). If I wanted to publish this, I’d do more hand-checking and work on the detector. Also, attribution is a guess: I think that the convention is that buyers counsel drafters in public deals, and the parties share it in private ones, and the evidence here is consistent with that story, but I don’t observe it directly.

This is so interesting and I hope you expand into a full paper. I wrote about boilerplate language in filings, probably same lawyer drafted, when we were experiencing pandemic era proliferation of “pricing power”. https://thedig.substack.com/p/when-companies-tell-you-how-they